Healthcare procurement BPO to hit $11Bn by 2030: report

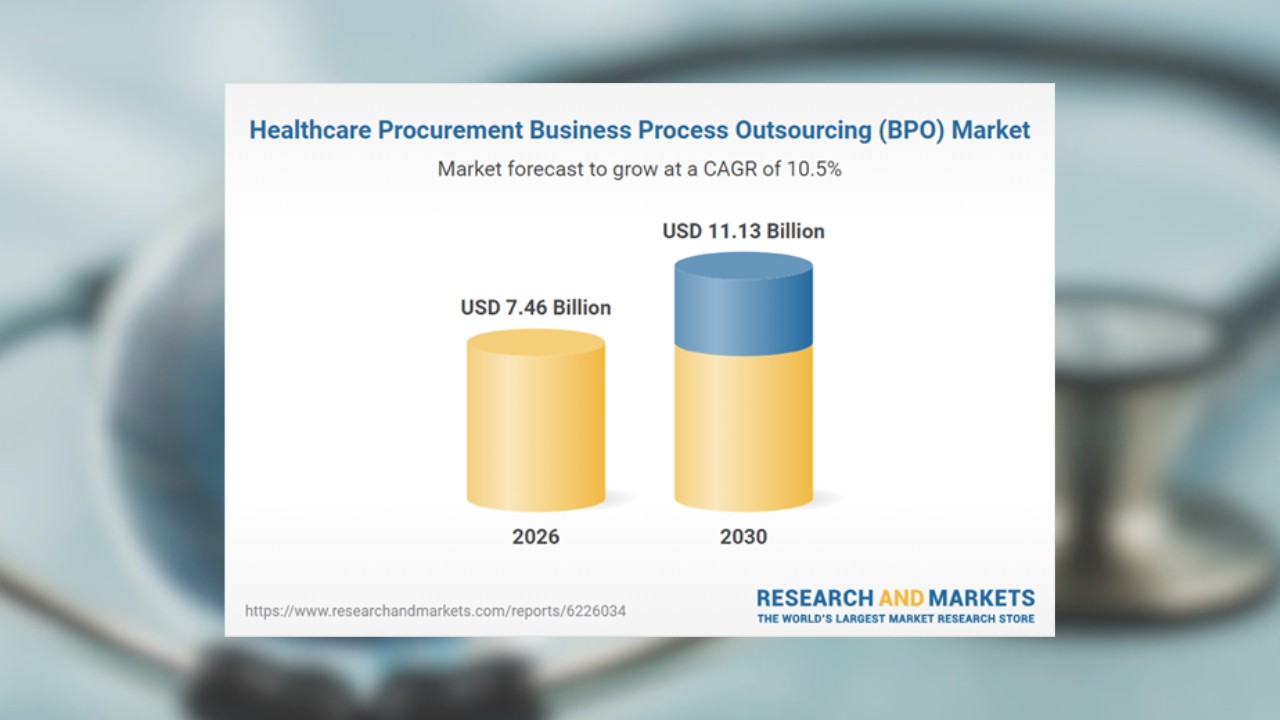

DUBLIN, IRELAND — Global healthcare procurement BPO reached $7.46 billion in 2026 and is forecast to hit $11.13 billion by 2030, growing at a 10.5% compound annual rate (CAGR), according to a new market report from Research and Markets.

The trajectory is driven by health systems worldwide shifting pharmaceutical and medical supply chain procurement to specialized third-party operators as complexity and cost pressure outpace what internal procurement teams can manage.

Healthcare procurement BPO hits $11Bn by 2030

The market — valued at $6.73 billion in 2025 before rising 10.8% in 2026 — spans six service lines: category management, sourcing, procurement transformation, transaction management, supplier management, and related services, delivered to hospitals, clinics, pharmaceutical companies, and healthcare providers across both cloud-based and on-premise deployments.

North America held the 2025 market lead, while Asia-Pacific — driven by China, India, and Japan — is the fastest-growing region, as rising government healthcare expenditure and scaling hospital networks in emerging markets generate procurement management demand that internal administrative capacity cannot absorb.

The 10.5% CAGR from 2026 to 2030 positions healthcare procurement BPO as one of the fastest-growing segments in health services outsourcing — outpacing the broader BPO sector’s average growth rate and reflecting the compounding cost of managing pharmaceutical and medical supply procurement without dedicated specialist infrastructure.

“The market is poised to reach $11.13 billion by 2030 at a CAGR of 10.5%,” The Business Research Company stated in its Healthcare Procurement BPO Global Market Report 2026.

Asia-Pacific growth opens procurement BPO beyond mature markets

The market’s core growth drivers are cost containment pressure, supply chain complexity in pharmaceutical and medical device procurement, and the adoption of digital tools — automation, cloud-based analytics, and supplier management platforms — that specialist BPO operators deploy faster than in-house health system teams building equivalent capability from scratch.

Major operators include Genpact, EXLService Holdings, and WNS Holdings on the BPO delivery side alongside procurement technology platforms GEP, Coupa Software, JAGGAER, Ivalua, and Global Healthcare Exchange — with IBM, PwC, EY, Infosys, HCL Technologies, Wipro, and Tech Mahindra competing for enterprise health system mandates across both BPO delivery and technology deployment.

Hospitals and health systems are the primary end-user base, with pharmaceutical companies expanding outsourced procurement as the volume and prior authorization complexity of medical supply category management outpaces what internal functions can handle cost-effectively at scale.

For Philippine and Indian BPO operators with established healthcare delivery practices, the $11.13 billion 2030 projection represents a procurement services pipeline adjacent to revenue cycle and clinical support categories they already serve — with Asia-Pacific’s fastest-growing regional status signaling that enterprise health clients are now actively outsourcing procurement functions alongside higher-complexity BPO.

“Healthcare supply chain complexities and rising pharmaceutical demand are creating sustained outsourcing pressure that digital procurement specialists are positioned to absorb more efficiently than internal health system teams,” the report noted.

For BPO operators tracking healthcare services specialization, the market’s 10.5% CAGR through 2030 documents that health systems are treating procurement outsourcing as a strategic operating decision — one sustained by pharmaceutical and medical supply chain complexity that internal functions cannot replicate at comparable cost.