Insurance-as-a-Service market to hit $624Bn by 2034: Market.us

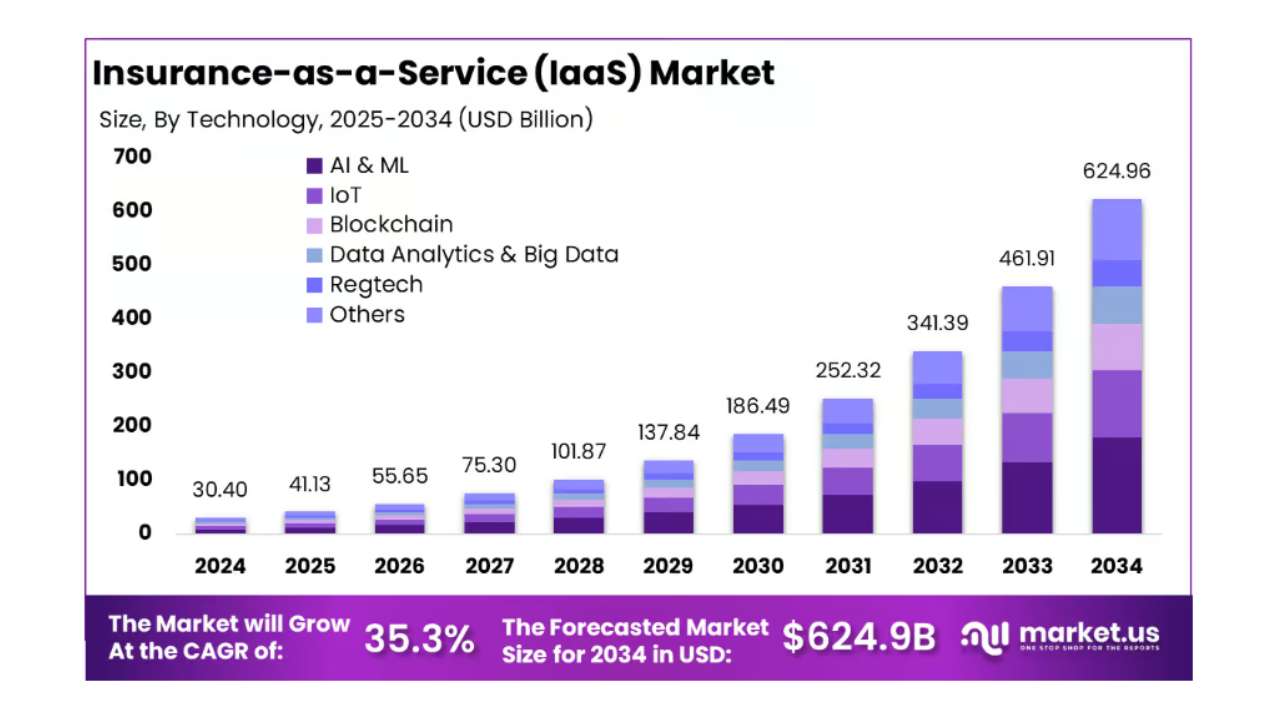

NEW YORK, UNITED STATES — The global Insurance-as-a-Service (IaaS) market is poised for explosive growth, projected to surge from $30.4 billion in 2024 to $624.9 billion by 2034 at a 35.3% compound annual growth rate (CAGR), according to Market.us.

North America is now on the front line, controlling 39.4% of the market, which can be attributed to cloud-based solutions, adoption of AI, and the desire to embed insurance products in digital environments.

Digital adoption reshapes insurance

The prevalence of API facilitations in the region has made it a dominant region, which has led insurers to prioritize coverages in the background of e-commerce, mobility, and fintech applications.

Of those, approximately $9.6 billion in revenue in the United States is driven by what we believe is the legacy insurers’ ability to enable operations to move to the cloud with cloud-native solutions, which is increasing at a 32.6% CAGR.

Among the critical trends are AI-driven underwriting and claims automation, which allow for decreasing processing time and improving the customer experience.

Insurers are increasingly focusing on software solutions, which occupy 76.5% of the market, to replace outdated systems. General insurance leads the way in software implementation, accounting for 56.7%, due to the need for flexible, scalable products.

AI and embedded insurance unlock growth

One of the emerging trends is the concept of embedded insurance, which is built into travel booking, retail, or even gig economy applications, thereby removing friction from a typical distribution scheme.

It is also opening up a lucrative market to non-insurance companies, including fintechs and e-commerce players, that can sell customized coverage without developing in-house bespoke infrastructure to do so.

The challenges, however, have been regulatory barriers and the integration of legacy systems, especially on a global scale.

Tech giants and insurtechs battle for market share

IaaS, which is dominated by Cognizant, IBM, Salesforce, and other major players, but also reaches niche providers. Consulting firms like Accenture can bridge this gap by helping insurers transition their legacy systems.

Nonetheless, there is a shortage of tech talent, and the cost of modernization remains high, resulting in slow adoption despite competition. Insurers must balance innovation with meeting regulatory requirements, which are fragmented in the cross-border digital offering.